After a car accident in Austin, your primary focus is understandably on recovery. You seek medical treatment, hire a personal injury lawyer, and eventually reach a settlement with the at-fault driver’s insurance company. You see a settlement figure—perhaps $50,000 or $100,000—and assume that money is yours to cover your lost wages and pain and suffering.

Then comes the “hidden cost” that many victims never see coming: the medical lien.

Medical liens can quietly consume a significant portion—sometimes all—of a personal injury settlement. While your doctors and the hospitals provided the care you needed, the way they secure payment can feel like a secondary injury. Understanding how liens work in Texas, specifically within the Austin healthcare landscape, is critical to ensuring you actually take home the compensation you deserve.

What is a Medical Lien?

In the simplest terms, a medical lien is a legal claim filed by a healthcare provider against your personal injury settlement or judgment. It is a “right of payment” that attaches to your legal case. When a lien is in place, the insurance company paying your settlement is often legally obligated to pay the medical provider directly before you receive a dime.

Think of it like a mortgage on a house. You can’t sell the house and pocket all the cash without paying off the bank first. In a personal injury case, the “house” is your settlement, and the “bank” is the hospital or doctor who treated you.

Types of Liens in Texas

Not all liens are created equal. In Texas, they generally fall into five categories, each with different rules for enforcement and negotiation.

1. Hospital Liens (Statutory)

Under Chapter 55 of the Texas Property Code, a hospital has a statutory right to a lien if you are treated within 72 hours of an accident. This is the most powerful type of lien because it is backed by state law. If a hospital files this lien properly in the county records, the insurance company is legally “on notice” and must pay the hospital from the settlement proceeds.

2. Healthcare Provider Liens (Contractual)

Individual doctors, surgeons, or imaging centers may ask you to sign a “Contractual Lien.” Unlike hospitals, these providers don’t have an automatic law protecting them, so they make you sign a contract that gives them a legal interest in your case.

3. Health Insurance Subrogation

If your private health insurance (like Blue Cross Blue Shield or UnitedHealthcare) pays for your accident-related treatment, they usually have a “subrogation” clause in your policy. This allows them to seek reimbursement from your settlement for the bills they paid.

4. Medicare and Medicaid Liens

These are federal and state-level liens. If the government pays for your care, they have a “super lien.” Under the Medicare Secondary Payer Act, they have the first right of recovery, and their claims are notoriously difficult and slow to resolve.

5. Workers’ Compensation Liens

If you were injured on the job and workers’ comp paid your medical bills, they are entitled to be paid back from any settlement you reach with a third party (like a negligent driver) under Texas Labor Code §417.001.

How Liens Work in Austin Personal Injury Cases

When you are rushed to an Austin-area emergency room—such as St. David’s or Dell Seton Medical Center—the hospital’s billing department immediately goes to work. They check to see if the injury was caused by a motor vehicle accident.

If it was, many Austin hospitals will intentionally not bill your health insurance. Why? Because they can often collect 100% of their “chargemaster” rates (the high, un-discounted prices) through a lien, whereas health insurance would only pay them a small, contracted fraction of that amount.

The hospital will file a notice of lien in the county where the services were provided. Once filed, this lien is a public record. When the at-fault driver’s insurance company (like State Farm or GEICO) gets ready to pay your claim, they run a search for liens. If they find one, they will include the hospital’s name on the settlement check, or refuse to issue the check until the lien is resolved.

The Letter of Protection (LOP) Trap

If you don’t have health insurance or can’t afford your deductible, an Austin chiropractor or specialist might offer to treat you under a Letter of Protection (LOP).

An LOP is a document sent by your attorney to a medical provider, guaranteeing that the provider will be paid out of the final settlement. While LOPs are essential for getting care when you are broke and injured, they can be a trap if not managed correctly.

What they don’t tell you:

- Inflated Costs: Providers often charge significantly more for LOP-based treatment than they would for a cash-pay patient or an insurance patient.

- No Risk for the Doctor: The doctor gets to charge “premium” prices, and they know the attorney is responsible for protecting their bill.

- Your Personal Liability: If you lose your case, the LOP doesn’t disappear. You are still personally responsible for those high medical bills.

How Much Can They Claim? (Texas Lien Laws)

In Texas, a hospital lien is limited. Under the law, a hospital lien cannot exceed the amount of a “reasonable and regular rate” for the services. Furthermore, it cannot exceed 50% of the total settlement.

However, “reasonable and regular” is a subjective term. Hospitals often claim their full, undiscounted rates are reasonable, even if they routinely accept 20% of that amount from insurance companies. This is where the battle begins.

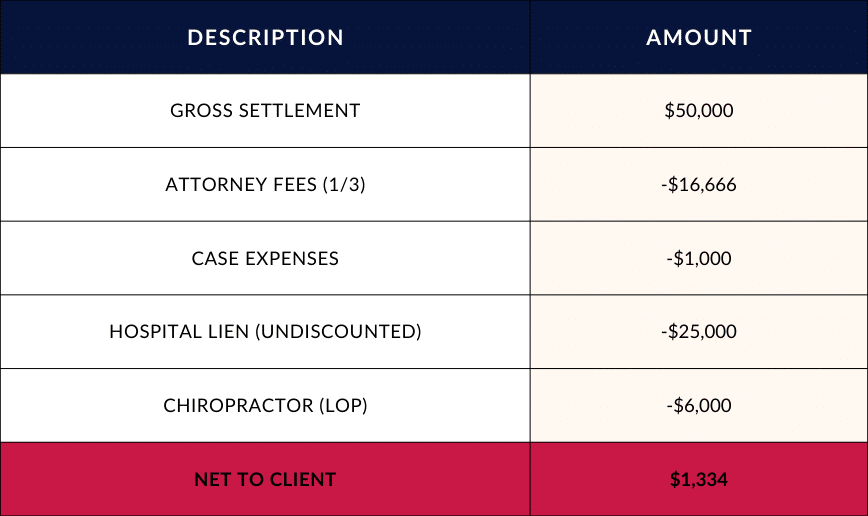

How Liens Reduce Your Settlement: An Example

Let’s look at how a lien can devastate a settlement if not negotiated.

In this scenario, the victim—who suffered the pain, the trauma, and the missed work—walks away with almost nothing, while the hospital and doctors take the lion’s share. This is exactly what we fight to prevent.

Negotiating Lien Reductions

The good news is that most liens are negotiable. Just because a hospital files a lien for $25,000 doesn’t mean they are entitled to all of it.

What’s Negotiable?

- Hospital Liens: We challenge the “reasonableness” of the charges. If the hospital charges $5,000 for a CT scan that usually costs $500, we fight to reduce it.

- Contractual Liens: These are often reduced based on the total settlement amount to ensure the client gets a fair share.

- Subrogation: Depending on whether your insurance plan is “ERISA-qualified” or not, we can often force a reduction based on the “Common Fund Doctrine,” requiring the insurance company to pay their share of the attorney’s fees.

Common Reduction Percentages

While every case is different, it is common to see liens reduced by 20% to 50%. In cases where the settlement is small (policy limits) and the bills are high, we often negotiate “pro-rata” distributions where the providers take a massive cut to ensure the client is compensated.

When Providers Won’t Budge

Occasionally, a provider—often a specific Austin-area surgical center or a “lien-funding” company—will refuse to reduce their bill. In these cases, your attorney must be prepared to litigate the reasonableness of the lien or use the Texas “Paid vs. Incurred” statute to challenge the validity of the bills in court.

The Attorney’s Role in Lien Resolution

Most people think a lawyer’s job ends when the settlement is signed. In reality, the most important work often happens after the settlement is reached. This is the “lien resolution” phase.

A skilled Austin personal injury attorney will:

- Verify the Lien: Ensure the hospital followed the strict filing requirements of the Texas Property Code. If they missed a deadline, the lien may be invalid.

- Audit the Bills: Look for double-billing or charges for treatment unrelated to the accident.

- Negotiate Aggressively: Use the “Made Whole Doctrine” and other legal arguments to force providers to lower their demands.

- Protect Your Credit: Ensure that as the liens are paid, the providers issue “Lien Releases” so these debts don’t haunt your credit score later.

Mistakes That Increase Your Lien Burden

To protect your settlement, avoid these common mistakes:

- Not using health insurance: If you have it, use it. Even if the hospital tells you they “don’t take it for accidents,” they are often lying. They want the lien because it pays more.

- Signing everything at the ER: Hospitals often tuck “Assignment of Interest” forms into the stack of intake papers.

- Waiting too long to hire a lawyer: By the time you hire a lawyer, a hospital may have already perfected their lien, giving you less leverage.

Real Case Example: The Power of Negotiation

We recently represented an Austin man in a “T-bone” collision where the insurance company initially denied all liability. Joe Lopez took immediate action, securing a temporary restraining order to inspect the vehicle and prove fault.

Our client had sustained a serious sternum fracture, resulting in significant medical bills. We secured a $100,000 policy limits settlement. While the gross amount was high, the client’s take-home pay depended entirely on our ability to manage the costs. After we negotiated the medical expenses and accounted for all legal fees, the client received a net recovery of $50,422.07.

By fighting the insurance company’s denial and carefully resolving the medical debt, we ensured the client walked away with a major portion of the settlement. See more case results here.

Contact Joe Lopez Law For a Free Case Evaluation

If you’ve been injured in Austin, don’t let medical providers dictate how much of your settlement you get to keep. Medical liens are complex, and the laws are designed to favor big hospitals—unless you have an advocate who knows how to fight back.

At Joe Lopez Law, we don’t just settle cases; we resolve the medical debt that comes with them. We handle the negotiations with hospitals, insurance companies, and Medicare so you can focus on your life.

Contact Joe Lopez today for a free case evaluation. We will review your medical bills and any liens filed against you to ensure you aren’t being overcharged.